The $5,000 Mistake: Why Calling Your Agent Before Filing a Claim Could Save You Thousands

Last month, a Spartanburg homeowner called me after their insurance company dropped them. The reason? Three small claims totaling less than $2,000 over two years. A 5-minute conversation before each claim could have saved their coverage and thousands in future premiums.

As a local insurance agent who’s been serving the Upstate South Carolina community for years, I see this scenario play out far too often. Homeowners might think they’re saving money by filing a claim any time insurance might pay out. In reality, they’re setting themselves up for a financial setback that could last years.

The Hidden Cost of Small Claims

Here’s what most homeowners don’t realize: every claim you file stays on your record for 3-5 years, and insurance companies use this history to determine your rates and whether they’ll even keep you as a customer.

Let me break down the real math:

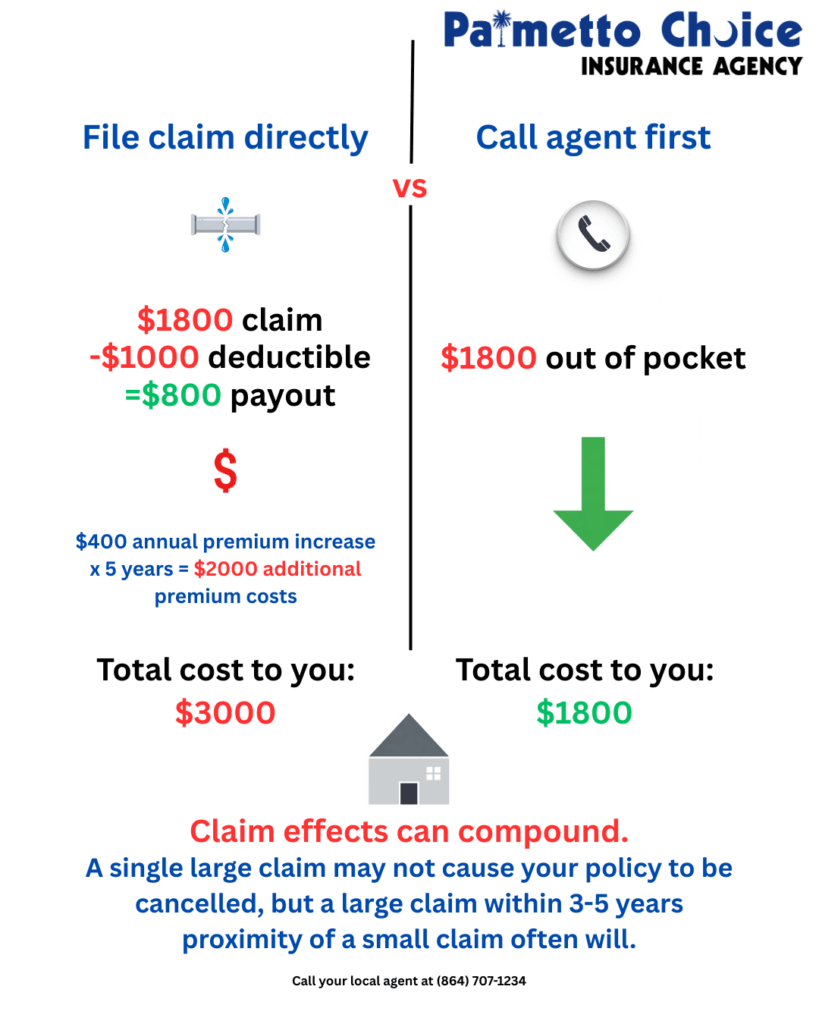

– File a $800 water damage claim today

– Your rates increase by $400/year for the next 5 years

– Total cost to you: $3,000 for an $800 repair

That’s not even counting what happens if you need to find new insurance after being dropped. In today’s market, that could mean paying 30-50% more with a different carrier.

Real Examples from Right Here in Spartanburg

The $750 Wind Damage Disaster

A client called last spring about roof damage from a storm. They were ready to file a claim until we did the math together. Their deductible was $1,000, so insurance wouldn’t pay a penny anyway. But filing that claim would have stayed on their record and likely increased their rates. They paid out of pocket and saved thousands in the long run.

The Three-Strike Story

Another homeowner filed three small claims in 18 months: a minor kitchen water leak ($900), storm damage to a fence ($650), and a small theft claim ($1,200). Total claims: $2,750. The result? Their insurance company non-renewed their policy, and their new premium was $1,800 higher per year. That’s $9,000 over five years for less than $3,000 in claims.

The $50 Mistake

One client filed a claim for what they thought was $1,500 in damage. After the adjuster’s visit, the actual covered damage was $950 – just $50 under their $1,000 deductible. Insurance paid nothing, but the claim still went on their record. Two years later, when they had a legitimate large claim, the company pointed to their “claims frequency” and raised their rates significantly.

The “Call First” Rule That Could Save You Thousands

Before you file any claim, ask yourself these questions – or better yet, call us and we’ll walk through them together:

1. Is it worth more than my deductible plus $1,000?

If your damage is $2,000 and your deductible is $1,000, you’ll only get $1,000 from insurance. But that claim could easily cost you $2,000+ in higher premiums over the next few years.

2. Can I afford to pay this myself?

Sometimes the smart financial move is to pay out of pocket now to avoid years of higher premiums.

3. Is this really covered?

Many homeowners file claims for things that aren’t actually covered, like gradual damage or maintenance issues. This wastes everyone’s time and still goes on your record as a claim.

4. How many claims have I filed recently?

Insurance companies look at frequency, not just dollar amounts. Multiple small claims can be worse than one large claim.

When You Should File a Claim

Don’t get me wrong – insurance is there for a reason. You should absolutely file claims for:

– Major COVERED damage over $5,000

– Liability situations where someone could sue you

– Damage you truly cannot afford to repair yourself

– Situations where waiting could make the damage worse

The Local Advantage

This is exactly why working with a local agent matters. When you call Progressive or Geico’s 1-800 number, the person on the other end doesn’t know you, doesn’t know your claims history, and certainly doesn’t care about your long-term financial picture. Their job is to process your claim, not protect your long-term interests.

When you call Palmetto Choice Insurance at (864) 707-1234, you’re talking to someone who knows your situation, understands the local market, and has a vested interest in keeping you as a happy, long-term client. We can walk through the pros and cons of filing a claim in about 5 minutes – and that conversation could save you thousands.

What to Do Right Now

If you’re dealing with potential damage to your home:

1. Document everything with photos and notes, but don’t file a claim yet

2. Get repair estimates to understand the true cost

3. Call us first at (864) 707-1234 to discuss whether filing makes financial sense

4. Remember: We’re on your side, and we want to help you make the smartest decision for your wallet

The Bottom Line

Insurance should protect you from financial catastrophe, not create it. A quick conversation with your local agent before filing a claim isn’t just good customer service – it’s potentially the most valuable 5 minutes you’ll spend all year.

At Palmetto Choice Insurance, we’ve been helping Spartanburg families make smart insurance decisions for over a decade. We’re not just here to sell you a policy; we’re here to help you use it wisely.

Before your next potential claim, give us a call at (864) 707-1234. A quick conversation could save you thousands.

—

Palmetto Choice Insurance Agency has been serving Spartanburg and the Upstate South Carolina community for decades. We represent over 50 insurance carriers to find you the best coverage at the best price. Visit us at 970 Howard St, Spartanburg, SC 29303, or request a quote online at www.palmettochoice.com.