That’s a lot of numbers…

Before every renewal, it comes…a large packet with 50, 60, maybe 100 pages. All the terms and conditions and definitions of your auto insurance policy, and then a huge string of numbers. To the average person, it’s probably kind of like a foreign language…most folks have a pretty good grasp on what their deductibles mean, but past that, it just a bunch of noise. Limits this, property damage that…odds are good you might just glaze over it.

Our focus today is going to be on your liability limits – which also impact your uninsured and underinsured motorist coverages. We’re going to break down what each number means.

Split limits vs. combined single limit

To begin with, auto policy limits of coverage can be expressed in two ways: split limits, or combined single limit.

Combined Single Limit

The simplest to understand is the combined single limit. The policy will display a simple limit of liability: for example, $100,000, or $300,000, or $500,000. The displayed limit is the most the policy will pay for all damages you are liable for – whether it’s for medical bills or car repairs. Payments can be applied without restrictions regardless of how the damages are broken down.

Split Limits

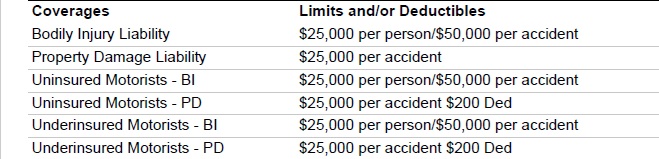

The vast majority of auto insurance policies, however, are written with split limits. You may see your policy show limits of 25/50/25, or 100/300/100, or 250/500/250. Each number represents a different limit.

Bodily Injury

The first number is the bodily injury limit per person. This means physical injury to a person. So if your auto policy has a bodily injury limit of $25k, then even if an injured person incurs $30k, or $70k, or even $100k in medical bills, the most the policy will pay is $25k for one person.

The second number is an aggregate limit. It is a PER ACCIDENT limit on bodily injury. So with 25/50/25 limits, the maximum the policy pays per person is $25k, and if the injured party’s vehicle had more than one occupant, the most it would pay for EVERYONE’s medical expenses is $50k – whether there are two passengers or six passengers, $50k is the absolute limit.

So for example, If Tom and Sue are rear-ended by someone with 25/50/25 limits, and Tom’s medical bills amount to $15k and Sue’s amount to $20k, since both incurred expenses less than the limit, both would be covered in full. If Tom received $20k in medical bills, and Sue received $35k, the auto policy would pay $20k to Tom, and $25k to Sue. Even though Tom’s expenses did not reach the limit, that per person limit cannot be applied to Sue’s medical bills, since she already exceeded the $25k per person limit. Now if they had two passengers in the back seat to add to that $20k and $25k, it only takes another $5000 to exceed the per-accident limit. At that point, all four passengers might receive significantly less than the $25k per-person limit, since the policy cannot pay out more than $50k total for injury to all affected individuals.

Property Damage

The third number in split limits is Property Damage – this defines the most the policy will pay for damage to another person’s property. While naturally your first response is that this might mean another person’s car, it also could mean damage to any property they own – personal belongings, a house, or even a fence or mailbox. Property damage coverage is not sub-divided the way personal injury is. It is a simple PER ACCIDENT limit of coverage. So whether you are responsible for hitting just one car, hitting someone’s car AND house, or even causing a 20-car pileup, the property damage limit shown is the most your policy would pay for property damage to ALL affected parties.

“State Minimum”

Every state has a different minimum (aka statutory) coverage limit. In South Carolina the minimum limits of coverage you can purchase for auto insurance is 25/50/25. This has been the minimum limit since 2007, when the minimum limits were increased in SC from 15/30/15 to 25/50/25. Currently, there is legislation being considered to increase these limits to 50/100/50. We don’t know yet when or if this measure will pass, but you can be sure this will be a time of tumult in the world of auto insurance. You can contact us at (864) 707-1234, Request a Quote online, or chat with us to ensure you’re properly covered at the best value.

Regardless of legal requirements, you should consider increasing your limits of coverage. See our blog post about Why You Should Increase Your Auto Insurance Liability Limits to see why we recommend this.